A home sale contingency is a clause in a real estate purchase agreement that makes buying a new home conditional on the buyer first selling their current property. Roughly 23% of buyers include this clause in their offers specifically to avoid carrying two mortgages at the same time. For San Diego buyers and sellers, understanding how this clause works, what it costs you in negotiating power, and how to manage it well can mean the difference between a smooth closing and a collapsed deal.

What is a home sale contingency and why does it matter?

A home sale contingency is defined as a contractual condition that voids a purchase agreement if the buyer cannot sell their existing home within a specified timeframe. The clause protects the buyer from a scenario most people dread: owning two homes, paying two mortgages, and scrambling to cover both sets of carrying costs.

The financial logic is straightforward. Most buyers need the equity from their current home to fund the down payment on the next one. Without a contingency clause, a buyer who fails to sell their existing property on time faces a brutal choice: breach the contract and lose their earnest money, or close on a home they cannot yet afford.

Earnest money typically runs 1 to 3% of the purchase price. On a $900,000 San Diego home, that is $9,000 to $27,000 at risk. The contingency clause is the mechanism that returns that deposit to the buyer if the sale of their current home does not happen by the deadline.

How does a home sale contingency work in practice?

The mechanics of a home sale contingency clause follow a defined sequence. Here is how the process typically unfolds:

- Offer submission. The buyer submits a purchase offer that includes the contingency clause, specifying that the deal closes only after their current home sells.

- Contract deadlines. The agreement sets two key dates. The first is the deadline by which the buyer must have a signed contract on their current home. The second is the drop-dead date, the final closing deadline for the entire transaction. These dates typically fall 30 to 60 days from the agreement signing.

- Kick-out clause activation. Sellers almost always require a kick-out clause that lets them continue marketing the property and accept stronger offers during the contingency period. If a better offer arrives, the original buyer gets 24 to 72 hours to waive the contingency or walk away.

- Concurrent closings. If the buyer's current home sells on time, both transactions close in sequence, often on the same day or within days of each other.

- Exit or proceed. If the buyer's home does not sell by the drop-dead date, the contingency allows them to exit the deal and recover their earnest money deposit.

Pro Tip: List your current San Diego home before you make an offer on a new one. Sellers take contingent offers far more seriously when you already have your property on the market. It signals preparation and reduces their perceived risk.

The synchronization challenge here is real. Aligning two settlement dates requires precise contract language covering what happens if financing fails late in the process. A single delay on either side can trigger a breach if the contract language is vague.

What types of home sale contingencies are there?

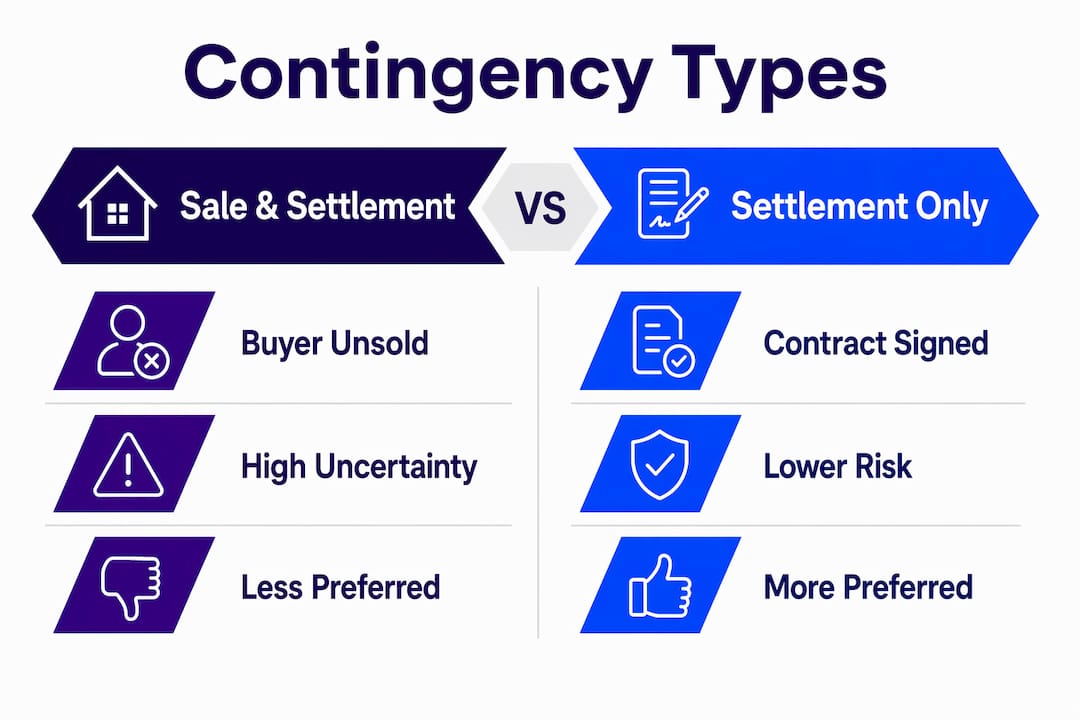

Not all home sale contingency clauses are identical. The two main types differ based on how far along the buyer is in selling their current home when they make the offer.

| Contingency type | What it means | Seller preference |

|---|---|---|

| Sale and settlement contingency | Buyer has not yet listed or has no signed contract on their current home | Lower preference; higher risk for seller |

| Settlement contingency | Buyer already has an accepted offer on their current home | Higher preference; deal is closer to closing |

A sale and settlement contingency carries more uncertainty because the buyer's current home has not yet attracted a buyer. The seller is essentially betting on two unknowns: whether the buyer's home will sell and whether it will sell in time.

A settlement contingency is a different situation entirely. The buyer already has a signed contract on their existing property. The only remaining variable is whether that deal closes as planned. Sellers clearly prefer this version because the risk window is much narrower.

In San Diego's competitive market, where well-priced homes in neighborhoods like Clairemont, North Park, or Carmel Valley routinely attract multiple offers, the type of contingency you bring to the table shapes how seriously a seller considers your offer.

What are the pros and cons of using a home sale contingency?

Home sale contingencies offer real protection, but they come with trade-offs that every San Diego buyer and seller should understand before signing anything.

Advantages for buyers:

- Financial protection against owning two homes simultaneously

- The ability to recover earnest money if the sale falls through

- Confidence to make an offer without having already sold your current home

- Reduced pressure to accept a lowball offer on your existing property just to meet a deadline

Disadvantages for buyers:

- Contingent offers are weaker in competitive markets because sellers prefer the certainty of non-contingent buyers

- Risk of losing the desired home if a stronger offer triggers the kick-out clause

- Complex timeline management that leaves little room for error

- Potential for the deal to collapse entirely if either transaction hits a snag

Pro Tip: If a San Diego seller rejects your contingent offer, consider a bridge loan or a home equity line of credit (HELOC) as a short-term financing alternative. These tools let you buy the new home before your current one sells, removing the contingency entirely and making your offer far more competitive.

Alternatives like bridge loans, HELOCs, or short-term rentals exist precisely because contingencies weaken buyer leverage in fast-moving markets. Renting temporarily after selling your current home gives you clean, non-contingent buying power. That flexibility often translates directly into a better purchase price. You can also review maximizing your home sale value to position your existing property for the fastest possible sale.

How to manage home sale contingencies effectively in San Diego

Managing a home sale contingency well requires coordination, clear contract language, and backup plans. Here is what buyers and sellers in San Diego should prioritize:

For buyers:

- List your current home before making an offer. Sellers favor buyers who have already taken this step because it demonstrates seriousness and reduces the seller's exposure.

- Work with an agent who has handled concurrent closings in San Diego before. The local market moves fast, and an experienced agent will draft contingency language that protects you without making your offer look weak.

- Have a backup plan ready. Without bridge loans or HELOCs, buyers relying solely on contingencies risk losing earnest money or being forced into a closing they cannot fund.

- Avoid common pitfalls by reviewing what not to do when buying a home before you finalize your offer strategy.

For sellers:

- Always include a kick-out clause when accepting a contingent offer. This preserves your right to accept a better deal if one arrives.

- Evaluate the buyer's current home situation carefully. A buyer with an accepted offer already in hand is a far safer bet than one who has not yet listed their property.

- Set realistic deadlines. Overly tight timelines pressure buyers into mistakes and can kill deals that would otherwise close cleanly.

- Price your home accurately from day one. A well-priced San Diego property sells faster, which directly reduces the contingency risk for everyone involved.

Managing two concurrent closings is genuinely complex. Buyers consistently underestimate how many moving parts are involved, and backup plans are not optional. They are the difference between a successful close and a financial setback.

How contingencies affect negotiation and the closing process

Home sale contingencies shift the power dynamic in a negotiation in ways that are not always obvious at first. Here is how the process typically plays out once a contingent offer is accepted:

- Seller leverage increases. The kick-out clause gives the seller ongoing leverage throughout the contingency period. They can continue showing the home and use any competing interest to pressure the buyer into waiving the contingency sooner than planned.

- Buyer communication becomes critical. Buyers must keep the seller informed about progress on their current home sale. Silence creates anxiety and can motivate a seller to accept a competing offer the moment the kick-out window opens.

- Closing timelines stretch. A contingent deal almost always takes longer to close than a standard transaction. Both parties need to build that reality into their moving plans, lease agreements, and financing arrangements.

- Late-stage risk spikes. Specific contract language covering financing failures and expiration dates is critical. A deal that falls apart two weeks before closing due to vague contingency language is far more damaging than one that never started.

- Momentum requires active management. Contingencies are not free passes. Real estate professionals consistently emphasize that agent guidance is what keeps these transactions on track when complications arise.

The negotiation dynamic in San Diego is particularly sensitive. In high-demand zip codes, sellers receive multiple offers within days of listing. A contingent offer that arrives alongside two non-contingent offers is almost always at the back of the line unless the buyer has done everything possible to strengthen their position.

Key takeaways

A home sale contingency protects buyers from financial exposure, but it requires precise timeline management, strong contract language, and backup financing plans to succeed.

| Point | Details |

|---|---|

| Core definition | A home sale contingency makes buying a new home conditional on selling the buyer's current property first. |

| Two contingency types | Settlement contingencies are safer for sellers; sale and settlement contingencies carry higher risk for both parties. |

| Kick-out clause reality | Sellers can accept competing offers during the contingency period, giving buyers just 24 to 72 hours to respond. |

| Earnest money exposure | Deposits of 1 to 3% of the purchase price are at risk if the contingency is not managed carefully. |

| Backup plans are required | Bridge loans, HELOCs, and temporary rentals reduce dependency on the contingency and strengthen buyer offers. |

What I've seen working contingencies in San Diego

After working with buyers and sellers across San Diego, I can tell you that the biggest mistake people make with home sale contingencies is treating them as a safety net rather than a contract obligation with real consequences.

Contingencies are not guaranteed escape routes. They are contractual exit ramps that only work if you manage the timeline actively and honestly. I have seen buyers lose their earnest money because they assumed the contingency would protect them even after they missed a key deadline. It does not work that way.

The sellers I work with in San Diego are sophisticated. They know the difference between a buyer who listed their home last week and a buyer who is still "thinking about it." Transparency matters. If you are bringing a contingent offer, come prepared with your current home already on the market, a realistic timeline, and a backup financing option in your back pocket.

The buyers who navigate contingencies successfully treat the process like a project with two parallel tracks. They stay in constant communication with their agent, their lender, and the seller's team. They have a bridge loan pre-approved before they need it. And they price their current home to sell fast, not to squeeze out every last dollar at the expense of timing.

If you are working with an agent who has not handled multiple concurrent closings in San Diego, that is a problem worth solving before you sign anything. Local market knowledge and contingency experience are not interchangeable with general real estate knowledge.

— Jeff

Ready to navigate your San Diego home sale with confidence?

Buying or selling a home in San Diego with a contingency in play is manageable when you have the right guidance from the start. Jeffsellssandiego works with buyers and sellers across San Diego to structure contingency offers that protect your interests without costing you the deal.

Whether you are searching for your next home or preparing to list your current property, Jeffsellssandiego provides the local expertise and hands-on support to keep both transactions on track. Browse current San Diego home listings to see what is available right now, or explore the buyer's guide for a full breakdown of the purchase process. You can also review the seller's guide to understand how to position your current home for the fastest, strongest sale possible.

FAQ

What is a home sale contingency in simple terms?

A home sale contingency is a clause in a purchase contract that lets a buyer cancel the deal and recover their earnest money if they cannot sell their current home by a specified deadline.

Are home sale contingencies common in San Diego?

Roughly 23% of buyers nationally use home sale contingencies. In competitive San Diego neighborhoods, they are less common because sellers typically prefer non-contingent offers.

What is the difference between a sale and settlement contingency vs. a settlement contingency?

A sale and settlement contingency means the buyer has no signed contract on their current home yet. A settlement contingency means the buyer already has an accepted offer, making it far less risky for the seller.

Can a seller accept another offer during a home sale contingency?

Yes. Sellers almost always include a kick-out clause that allows them to accept a competing offer. The original buyer then has 24 to 72 hours to waive the contingency or exit the deal.

What happens to earnest money if a home sale contingency is not met?

If the buyer's current home does not sell by the contract deadline and the contingency is properly written, the buyer recovers their full earnest money deposit. Without clear contingency language, that deposit can be at risk.