If you think the price on a listing or an offer is what determines a home's value, you're not alone. Most buyers and sellers in San Diego are surprised to learn that an independent third party has the final say. The role of home appraisal in sales goes far beyond confirming a number. It shapes loan approval, negotiation power, and whether a deal actually closes. This guide breaks down exactly how appraisals work, what they mean for your transaction, and what's happening right now in the San Diego market that every buyer and seller needs to know.

Table of Contents

- Key takeaways

- The role of home appraisal in sales, explained

- Why lenders require appraisals

- How appraisals affect buyers and sellers in real deals

- Appraisal gaps and San Diego's 2026 market reality

- Preparing for a successful appraisal in San Diego

- My take on appraisals after years in San Diego real estate

- Work with someone who knows the San Diego market

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Appraisals set the real value | A licensed appraiser's opinion of value, not the listing price, anchors what a lender will finance. |

| Lenders rely on appraisals heavily | Appraisal value determines loan approval, down payment requirements, and PMI eligibility. |

| Low appraisals trigger options | Buyers can renegotiate, cover the gap in cash, or walk away using an appraisal contingency. |

| San Diego has active appraisal gaps | Thin comparable sales pools and climate-related factors are widening the gap between contract prices and appraisals in 2026. |

| Preparation matters for sellers | Documenting upgrades and understanding local comps before the appraisal visit can meaningfully influence your outcome. |

The role of home appraisal in sales, explained

The formal term for what most people call a "home appraisal" is a real property appraisal. It is an independent, professional estimate of a property's fair market value conducted by a licensed or certified appraiser. This is not the same as a home inspection, a Zestimate, or an agent's pricing opinion. The appraiser works for no one involved in the deal.

Home appraisers are licensed professionals trained to estimate market value using uniform standards and verifiable data, including education requirements, licensing exams, and adherence to Uniform Standards of Professional Appraisal Practice (USPAP). That independence is intentional and legally protected.

Here is what the home appraisal process actually involves:

- Physical inspection: The appraiser visits the property and documents its size, layout, condition, features, and any visible issues.

- Data collection: They record square footage, number of bedrooms and bathrooms, lot size, garage, pool, and any upgrades.

- Comparable sales analysis: They pull recent sales of similar homes in the area, typically within the past six months and within a defined geographic radius, to establish what buyers have actually paid.

- Final value estimate: They reconcile all data into a written report that assigns a specific dollar value to the property.

The real skill in the role of home appraiser is balancing objective data with judgment calls. Two homes on the same block with identical square footage may appraise differently based on layout, renovation quality, and condition. Appraisers combine physical inspection with market data to produce a figure that reflects what a reasonable buyer would pay in a competitive, open market.

Pro Tip: If you are a seller, walk the appraiser through any upgrades you have made. They cannot guess that your HVAC system is brand new or that you just replaced the roof. A one-page summary with dates and costs goes a long way.

Why lenders require appraisals

A mortgage lender is not handing you money out of goodwill. The home is collateral. If you stop making payments, the lender needs to recover its money by selling the property. Lenders require appraisals to confirm that the home's value sufficiently protects their loan investment against the risk of foreclosure loss.

This is why the appraisal process is lender-ordered and borrower-paid. The lender selects the appraiser, often through an appraisal management company, specifically to prevent anyone from pressuring the appraiser toward a higher number. Appraisal independence rules are enforced under the Truth in Lending Act and Regulation Z, which prohibit buyers, sellers, and agents from influencing the appraiser's conclusion.

Here is how the appraised value directly affects your loan:

- Loan-to-value ratio (LTV): Your lender calculates LTV based on the appraised value, not the purchase price. A higher LTV means more lender risk.

- Loan approval: If the appraisal comes in below the purchase price, the lender may only finance based on the lower appraised value.

- Down payment: You may need to bring more cash to closing to cover the difference between the loan amount and the purchase price.

- Private mortgage insurance (PMI): Appraised value determines home equity and PMI eligibility; a lower appraisal can push your equity below the 20% threshold.

- Closing timeline: If appraisal deadlines are missed before closing, lenders must postpone closing or obtain valid waivers under federal regulation.

The appraisal influence on sales is most visible in this lender relationship. Even a deal where both buyer and seller agree on price can collapse if the appraisal does not support the financing.

How appraisals affect buyers and sellers in real deals

This is where the real estate appraisal role gets personal. When an appraisal comes in at or above the contract price, everything moves forward smoothly. When it comes in low, the transaction hits a fork in the road.

A low appraisal can force buyers to renegotiate price, cover the shortfall in cash, or cancel the contract entirely. The protection that gives buyers this flexibility is called an appraisal contingency. Most purchase contracts in California include one by default, but buyers can and sometimes do waive it to compete in a hot market. Waiving that contingency means agreeing to cover any gap between the appraised value and the purchase price out of pocket.

When a low appraisal hits, these are the realistic options on the table:

- Renegotiate the price: The seller agrees to reduce the purchase price to the appraised value. This is the cleanest outcome but requires seller cooperation.

- Buyer covers the gap: The buyer brings additional cash to make up the difference. This works if the buyer has the funds and wants the property badly enough.

- Split the difference: Seller and buyer each absorb a portion of the gap. This is common in competitive markets where neither side wants to lose the deal.

- Cancel the contract: If the buyer has an appraisal contingency and cannot or will not cover the gap, they can walk away and recover their earnest money deposit.

How appraisals affect selling from the seller's side is equally significant. A seller who priced their home based on gut feel or a neighbor's sale three months ago may find the appraisal delivers an uncomfortable reality check. Worse, an appraisal shortfall can add days or weeks to a closing as parties renegotiate, which creates stress and sometimes new buyer cold feet.

Pro Tip: Sellers, if you receive a low appraisal and believe it is wrong, ask your agent to pull the comps the appraiser used. If there are recent sales that were missed or if square footage was measured incorrectly, you have grounds to request a formal reconsideration of value.

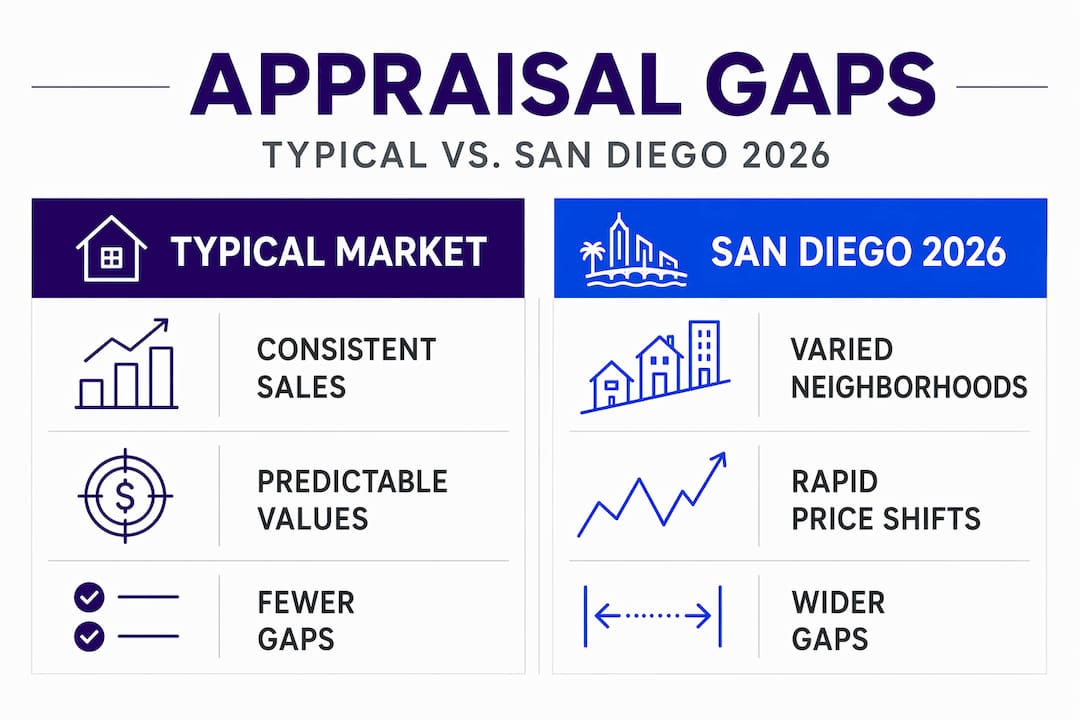

Appraisal gaps and San Diego's 2026 market reality

San Diego is not a simple market to appraise. The combination of coastal property variation, neighborhood-by-neighborhood price swings, and limited inventory creates real challenges for appraisers trying to find accurate comparable sales.

The 2026 appraisal gap is growing in markets like San Diego due to thin comparable sales pools, climate-related property risks, and the limitations of data-heavy automated valuation models. When comps are scarce or outdated, appraisers face a genuine dilemma: they cannot fabricate data, but the market may have moved faster than the sales record reflects.

Measurement inconsistencies in gross living area (GLA) reporting add another layer of complexity. Differences in how above-grade versus below-grade square footage is recorded can materially shift the final appraised number, affecting underwriting and sale closings.

"2026 appraisal gaps require both lenders and borrowers to proactively build negotiation and risk mitigation strategies into deals, anticipating potential low or high valuations." — HousingWire

Here is how the current environment compares to typical market conditions for San Diego buyers and sellers:

| Factor | Typical market | 2026 San Diego reality |

|---|---|---|

| Comparable sales availability | Sufficient recent sales nearby | Thin pools, especially in coastal or luxury segments |

| Automated valuation accuracy | Generally reliable as a starting point | More variation due to rapid price shifts and limited data |

| Appraisal gap frequency | Occasional and manageable | More common, requiring active negotiation strategies |

| GLA measurement risk | Low if records are consistent | Higher where older records or additions exist |

| Climate risk adjustments | Rarely factored in | Increasingly part of valuation in wildfire and flood zones |

For San Diego buyers and sellers, the practical takeaway is this: build your expectations and your contracts around the possibility of an appraisal gap. It is not a sign that something went wrong. It is a feature of a fast-moving, supply-constrained market.

Preparing for a successful appraisal in San Diego

Whether you are selling or buying, you are not powerless in the home appraisal process. There are real steps both sides can take to influence outcomes or respond constructively when things do not go as planned.

For sellers, here is how to set up the strongest possible appraisal:

- Prepare a written summary of improvements. List every upgrade with the year completed and approximate cost. New kitchen, updated bathrooms, new roof, HVAC systems, and permitted additions all add value but only if the appraiser knows about them.

- Clean and declutter before the visit. Condition matters. An appraiser is making a professional judgment and a well-maintained home signals care and value.

- Pull your own comps in advance. Ask your agent to identify the strongest comparable sales in your neighborhood. If something is missing from the appraiser's report, you can submit it as part of a reconsideration request.

- Check your permit records. Unpermitted additions are a liability. Know what is on record and be prepared to discuss any discrepancies, especially around square footage.

For buyers, the importance of appraisals shows up most when results come in unexpectedly. Review the appraisal report carefully when you receive it. Look at the comps that were used, check the square footage against listing data, and ask your agent if anything looks off. Working with experienced buyers navigating the local market and appraisal processes can make the difference between losing a deal and closing one.

Requesting a reconsideration of value is a formal process and lenders treat it seriously. You need documented evidence, not just a feeling that the appraiser was wrong. Supply missed comparable sales, correct factual errors, or flag GLA measurement issues with supporting data.

Pro Tip: Avoid common appraisal mistakes like failing to be present or available during the visit, ignoring deferred maintenance, or assuming automated online estimates reflect appraised value. They almost never match.

My take on appraisals after years in San Diego real estate

I have watched clients lose deals, leave money on the table, and panic unnecessarily over appraisals. Here is what I actually believe after working through hundreds of transactions in this market.

Most people treat appraisals like a verdict. They do not. An appraisal is one professional's opinion of value based on available data at a specific point in time. I have seen appraisals come in low on homes that sold for over asking again three months later. The market does not always agree with the appraiser, and that tension is especially real in San Diego right now.

The biggest misconception I encounter is that a low appraisal means a buyer overpaid or a seller overpriced. Sometimes that is true. But often it simply means the comp pool is thin or an appraiser was overly conservative in a neighborhood they do not work in frequently. In those cases, a well-documented reconsideration of value actually works.

What I have learned is that preparation and knowledge reduce surprises dramatically. Sellers who walk into an appraisal with a clean home, a documented upgrade list, and an agent who has pre-pulled the strongest comps almost always get a better result than those who leave it to chance. For buyers, understanding what to avoid when buying, including waiving your appraisal contingency blindly in a competitive situation, protects you from costly mistakes.

Appraisals are not a hurdle. They are information. The sellers and buyers who use that information strategically come out ahead.

— Jeff

Work with someone who knows the San Diego market

Appraisals can make or break a deal, and having the right agent in your corner changes the outcome. At Jeffsellssandiego, I work with both buyers and sellers across San Diego, helping clients prepare for appraisals, respond to gaps, and negotiate with real knowledge of local market conditions.

If you are buying, explore the current San Diego listings and find properties matched to your goals. If you are selling, learn how to maximize your home's sale value before the appraiser ever walks through the door. Whether you are just starting out or already in contract, reach out to Jeffsellssandiego for guidance tailored to where you are in the process.

FAQ

What is the role of a home appraisal in a property sale?

A home appraisal provides an independent estimate of a property's fair market value. It protects lenders, informs buyers and sellers, and can determine whether a sale closes at the agreed price.

What happens if the appraisal comes in below the purchase price?

A low appraisal gives buyers with an appraisal contingency the option to renegotiate the price, cover the difference in cash, or cancel the contract and recover their earnest money deposit.

How does the appraiser determine home appraisal value?

Appraisers conduct a physical inspection and review comparable recent sales in the area. They balance objective data on size and condition with market evidence to produce a final value estimate.

Can a seller challenge a low appraisal?

Yes. A seller or buyer can submit a formal reconsideration of value with documented evidence such as missed comparable sales, factual errors in the report, or square footage discrepancies. The appraiser is not required to change the value but must review the submission.

Why is the appraisal gap a concern in San Diego in 2026?

San Diego's limited inventory and fast-moving prices create thin comparable sales pools. This makes it harder for appraisers to find recent, accurate data, which increases the chance that appraised values lag behind current contract prices.