If you're selling a house with HOA membership attached, you probably have questions. Can the HOA block your sale? What documents do you need? How much will it cost you at closing? The role of HOA in selling is widely misunderstood, and that misunderstanding causes real financial pain and transaction delays. The short answer: HOAs don't block sales directly, but they control a set of documents, fees, and compliance requirements that can absolutely derail a closing if you ignore them.

Table of Contents

- Key Takeaways

- The role of HOA in selling: what you actually need to know

- Estoppel and resale certificates explained

- How HOA fees and rules affect your sale price

- HOA-related delays that can slow your closing

- Practical steps for sellers managing HOA requirements

- My take on HOA as a seller: what I've learned

- Ready to sell in San Diego? Let's handle the HOA side together

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| HOAs don't block sales | HOAs rarely prevent a sale outright, but they enforce compliance and financial clearance before closing. |

| Order certificates early | Estoppel and resale certificates take 10 to 15 business days and must be ordered the moment your contract is firm. |

| Outstanding dues reduce proceeds | Any unpaid HOA balances get settled at closing, directly lowering your net proceeds. |

| Violations can kill deals | Unresolved HOA violations or unapproved modifications can trigger buyer demands or contract cancellations. |

| HOA health affects buyer financing | Lenders scrutinize HOA financial health, and a poorly managed HOA can complicate loan approvals for your buyers. |

The role of HOA in selling: what you actually need to know

A homeowners association governs the community you live in. It enforces covenants, conditions, and restrictions (CC&Rs), maintains shared amenities, and collects monthly dues to fund operations. When you decide to sell, the HOA doesn't become your adversary. It becomes an administrative layer you have to work through.

Here's what the HOA actually provides during a sale:

- Disclosure package. This bundle includes the CC&Rs, bylaws, rules and regulations, financial statements, meeting minutes, and reserve fund disclosures. Buyers review this to understand what they're agreeing to live under.

- Resale or estoppel certificate. This is a snapshot of your financial standing with the HOA, covering dues owed, pending assessments, fines, and any active liens.

- Membership confirmation. Sellers must formally disclose HOA membership and all related financial obligations. In most states, this is a legal requirement, not a courtesy.

State laws vary significantly on what's required and when. In Texas, for example, sellers must provide an HOA membership notice and a resale certificate with the buyer's contract, with certificate preparation costs running up to $375. Every state has its own timeline and document list, so knowing your state's rules before you list is non-negotiable.

Pro Tip: Review your seller obligations guide before listing so you understand exactly which HOA documents apply to your transaction and who is responsible for ordering and paying for them.

Estoppel and resale certificates explained

This is where sellers lose the most time and money through ignorance. An estoppel certificate (sometimes called a resale certificate depending on your state) is a legally binding financial statement from the HOA that tells the buyer exactly what is owed on the property.

Think of it this way. The certificate freezes a financial moment in time. It says your dues are current, or it says you owe $1,200 in back assessments and a $250 fine for that fence you painted without approval. Buyers and their lenders rely on this document to understand what financial baggage comes with the home.

Here's what the estoppel certificate typically covers:

- Current monthly dues amount

- Any past-due balances or delinquent assessments

- Pending special assessments not yet billed

- Active HOA liens on the property

- Unapproved modifications or open violations

Timing matters enormously here. Florida law requires estoppel certificates to be delivered within 10 business days of request. In Texas, resale certificates must be prepared no earlier than 60 days before delivery and updated within 180 days, which means a stale certificate can hold up or invalidate a transaction. Treat this document like a time-sensitive underwriting file, not administrative paperwork you'll get around to eventually.

Statistic: Estoppel processing times average 10 to 15 business days, with expedited options available for an added fee. Every day of delay pushes your closing date back.

Any outstanding dues the certificate reveals get paid directly out of your sale proceeds at closing. Sellers who pay off HOA balances before the closing statement is drafted avoid last-minute surprises that can rattle buyers and delay funding.

Pro Tip: Order your estoppel or resale certificate the moment your contract goes firm. Waiting even a few days can compress your closing timeline dangerously.

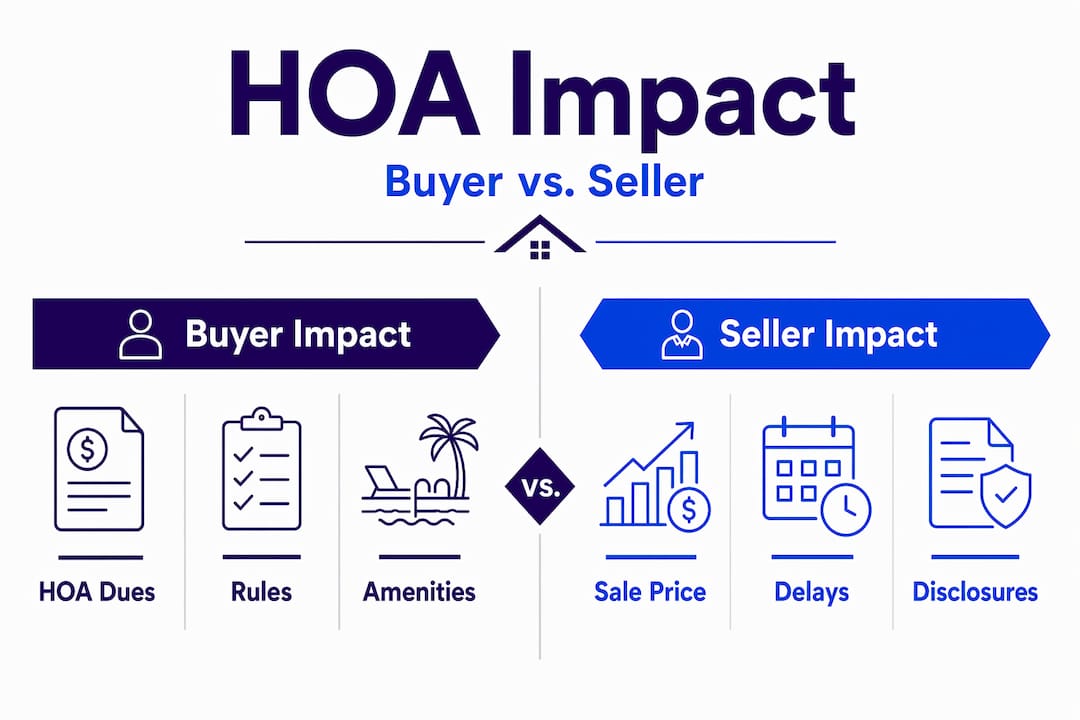

How HOA fees and rules affect your sale price

The impact of HOA on sales goes beyond paperwork. Monthly dues directly affect how much home a buyer can afford, which affects what they'll offer you.

Here's the practical math. If your HOA dues are $600 per month, that adds $7,200 per year to a buyer's carrying costs. At typical debt-to-income ratios, HOA fees reduce buyer purchasing power and can push a buyer's qualification threshold down significantly. In competitive markets, high dues price out otherwise qualified buyers and shrink your pool.

Beyond monthly dues, the following HOA factors shape buyer behavior and offers:

- Pending special assessments. A buyer who learns a $5,000 roof assessment is coming in 18 months will factor that into their offer, or walk away entirely.

- Low reserve funds. Lenders and savvy buyers read the financials. An HOA running on thin reserves signals deferred maintenance and future special assessments.

- Rental restrictions. If your HOA limits rentals, you've just eliminated investors and move-up buyers who want rental income flexibility.

- HOA financial health scrutiny. Fannie Mae and FHA have strict HOA financial health requirements. A troubled HOA can prevent buyers from getting conventional or government-backed loans on your property.

Here's a quick reference for how common HOA factors influence your sale:

| HOA Factor | Buyer Impact | Seller Impact |

|---|---|---|

| High monthly dues | Reduces purchasing power | Can lower offer price |

| Pending special assessments | Creates uncertainty | Demands concessions or price reduction |

| Low reserve fund | Flags future costs | Complicates lender approval |

| Rental restrictions | Narrows buyer pool | Reduces demand |

| Well-managed, amenity-rich HOA | Increases appeal | Supports higher list price |

A well-managed HOA with adequate reserves, moderate fees, and real amenities is genuinely a marketing asset. Sellers in those communities should highlight it, not apologize for it.

HOA-related delays that can slow your closing

Selling a house with HOA involvement introduces several specific bottlenecks most sellers don't anticipate until they're in the middle of a transaction.

The biggest delay trigger is the estoppel or resale certificate itself. Processing times routinely hit 10 to 15 business days even in normal circumstances. Add a holiday weekend, a management company that's slow to respond, or an expedited fee the seller didn't budget for, and you're looking at a closing date that slides.

But document timing isn't the only issue. Consider these common delay scenarios:

- Unresolved violations. Unapproved modifications and open violations discovered during the buyer's review can trigger remediation demands that pause the contract while repairs or reversals get completed.

- Stale or inaccurate certificates. If an estoppel certificate contains errors or goes past its validity window, it has to be reissued. That restarts the clock.

- HOA document delivery requirements. In Texas, mandatory HOA documents must be delivered as physical copies, not digital links. Sellers who miss this requirement face legal exposure and potential breach of contract claims.

- Right of first refusal clauses. These are rare, but CC&Rs occasionally contain right of first refusal provisions. Sellers need to confirm no active rights apply before marketing the property.

The coordination required between you, the HOA management company, the title company, and the buyer's lender is real work. None of these parties communicate automatically. You or your agent have to drive it.

Pro Tip: Before you list, pull your HOA account statement and confirm your standing. Knowing about violations or balances in advance gives you time to fix them on your schedule, not the buyer's.

Practical steps for sellers managing HOA requirements

Getting ahead of your HOA obligations before you list is the single most effective thing you can do to protect your timeline and net proceeds. Here's a clear sequence to follow:

- Contact your HOA or management company. Request a current account statement and a list of any open violations or pending assessments. Do this at least 60 days before you plan to list.

- Review all HOA documents. Read your CC&Rs and bylaws. Look for rental restrictions, approval requirements for modifications, and any pending litigation involving the HOA.

- Resolve all outstanding issues. Pay down any delinquent dues and address open violations before you list. Understanding HOA special assessments before you're in contract gives you time to negotiate or plan around them.

- Order the disclosure package. Know the cost and who pays it. In some markets, this is a seller expense. In others, it's negotiable.

- Order the estoppel certificate immediately when under contract. Do not wait. Pay the expedited fee if necessary.

- Use the HOA as a selling point when appropriate. If your community has great amenities, professional management, and healthy financials, put that in your marketing. Buyers who understand the HOA influence on home value will recognize a well-run community as a feature, not a liability.

Pro Tip: Factor HOA delinquency payoffs as a separate line item when estimating your net proceeds. Sellers who skip this step get unpleasant surprises on their closing statement.

My take on HOA as a seller: what I've learned

In my experience working with sellers across San Diego, HOA-related issues are one of the most consistent sources of transaction stress. Not because HOAs are adversarial, but because sellers underestimate how much administrative coordination they require.

I've watched deals nearly fall apart because a management company took 18 business days to issue an estoppel certificate that the seller didn't order until a week after going under contract. The buyer almost walked. The closing date pushed three weeks. It was entirely avoidable.

What I've found is that most sellers treat HOA obligations as an afterthought. They focus on staging, pricing, and inspections, which all matter, but they skip the pre-listing HOA audit entirely. That's where the real risk lives. A pre-listing HOA compliance audit catches violations, balances, and document gaps before they become a buyer's leverage point or a closing day crisis.

My honest recommendation: treat your HOA obligations as a core part of your listing strategy, not paperwork you'll handle once you have an offer. The sellers who do this close faster, with fewer concessions, and a lot less stress.

— Jeff

Ready to sell in San Diego? Let's handle the HOA side together

Navigating HOA rules for a home sale in San Diego requires local knowledge and attention to detail that generic advice simply can't provide. At Jeffsellssandiego, we walk sellers through every HOA-related requirement before the first showing, not after you're under contract and the clock is ticking.

From ordering disclosure packages and coordinating estoppel certificate timing to reviewing financials and resolving violations before they become buyer objections, Jeff handles the process so you don't lose time or money to administrative gaps. Whether you're just starting to think about listing or you're ready to move now, explore the seller resources or search available San Diego listings to see what the market looks like right now.

FAQ

Does an HOA have the power to block my home sale?

No. HOAs cannot block sales directly, but they can enforce liens and, in rare cases, exercise right of first refusal clauses. Resolving all dues and violations before closing prevents HOA-related interference.

What is an HOA estoppel certificate and why do I need one?

An estoppel certificate is a legally binding financial statement from the HOA confirming your dues, fines, and any liens on the property. Buyers and title companies require it before closing to confirm no hidden debts transfer with the home.

How long does it take to get an estoppel certificate?

Processing typically takes 10 to 15 business days, though expedited options are available for an additional fee. Order it immediately when your contract is firm to protect your closing date.

Can HOA fees affect whether my buyer qualifies for a mortgage?

Yes. HOA fees count toward a buyer's monthly debt obligations, which reduces how much home they can finance. A poorly managed HOA can also trigger lender restrictions that limit buyer financing options entirely.

What HOA documents do I need to provide when selling my home?

At minimum, sellers typically need to provide the CC&Rs, bylaws, rules and regulations, HOA financial statements, and an estoppel or resale certificate. State requirements vary, and in Texas, physical document delivery is legally required rather than electronic links.