Earnest money is defined as a good-faith deposit a buyer submits when making an offer on a property, signaling genuine intent to complete the purchase. The role of buyer's earnest money goes beyond a symbolic gesture. It protects the seller by compensating them if a buyer walks away without cause, and it gives the buyer a financial stake in following through. In San Diego's competitive market, understanding how this deposit works, how much to offer, and when you can get it back is knowledge that directly affects whether your offer wins or loses.

What is the role of buyer's earnest money in a transaction?

Earnest money functions as a handshake with financial backing, giving sellers real assurance that a buyer is serious. Without it, a seller would have no protection against a buyer tying up their property for weeks and then walking away on a whim. The deposit creates mutual accountability. The buyer has skin in the game, and the seller has a remedy if the deal falls apart without a valid reason.

The deposit is not an extra cost you pay on top of everything else. Earnest money is credited toward your cash-to-close at settlement, reducing the amount you need to bring to the table for your down payment or closing costs. Think of it as paying part of your purchase costs early. Understanding how it connects to your closing cost breakdown helps you plan your total cash needs accurately from day one.

A neutral third party holds the funds throughout the transaction. Escrow and title companies receive and hold earnest money deposits, protecting both buyer and seller until the deal closes or the contract is terminated. Neither party can simply pocket the money while a dispute is unresolved.

How much earnest money is standard in San Diego?

The standard earnest money deposit for residential real estate runs 1%–3% of the purchase price. On a $900,000 San Diego home, that means $9,000–$27,000 deposited upfront. That range reflects a national baseline. San Diego's low inventory and high demand regularly push expectations above that floor.

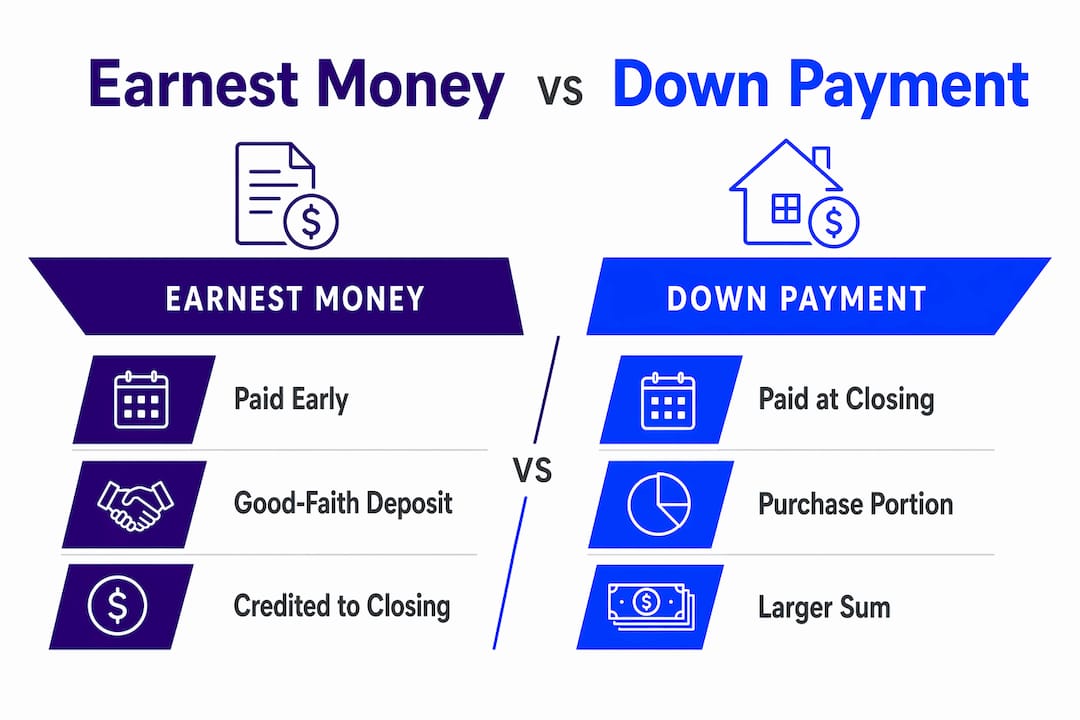

Here is how earnest money compares to the down payment, since buyers frequently confuse the two:

| Feature | Earnest money | Down payment |

|---|---|---|

| When paid | At offer acceptance | At closing |

| Purpose | Shows buyer commitment | Equity in the property |

| Held by | Escrow or title company | Lender or escrow |

| Refundable? | Yes, with valid contingency | Not applicable once paid |

| Applied to closing? | Yes, credited at settlement | Yes, part of cash-to-close |

The earnest money deposit is not separate from your down payment. It is a portion of it, paid earlier in the process.

Pro Tip: In San Diego neighborhoods like Point Loma or Downtown, where multiple offers are common, ask your agent what recent accepted offers used for earnest money. Local norms matter more than national averages.

When is earnest money refundable vs. forfeited?

Contingency clauses are the legal mechanisms that protect your deposit. The three most common are the inspection contingency, the financing contingency, and the appraisal contingency. Buyers are entitled to a full refund if they cancel within the contractually specified deadlines for any of these valid reasons. Miss a deadline, and that protection disappears.

Here is how the three main contingencies work in practice:

- Inspection contingency: You have the right to inspect the property and cancel if you find issues you cannot accept. Cancel before the deadline and your deposit comes back. Cancel after and you risk losing it.

- Financing contingency: If your loan falls through despite good-faith efforts to secure financing, you can exit the contract and recover your deposit. This protects buyers against lender denials outside their control. A mortgage contingency is one of the most important clauses in any purchase agreement.

- Appraisal contingency: If the property appraises below the purchase price and you cannot renegotiate, this contingency lets you exit without penalty.

If you back out without a valid contingency reason, the seller can keep your deposit as liquidated damages. Earnest money is a performance bond, not a fee. Forfeiture is the contractual consequence for a buyer who defaults without cause.

California adds a specific legal layer here. The California Residential Purchase Agreement requires both buyer and seller to initial the liquidated damages clause for the seller's retention of earnest money to be the exclusive remedy. If that clause is not initialed by both parties, the seller may pursue additional damages beyond the deposit. Always read and understand what you are initialing.

Pro Tip: Never waive a contingency verbally. Any contingency removal must be in writing and signed by both parties to be enforceable under California contract law.

How to use earnest money strategically in San Diego's market

San Diego's housing market rewards buyers who understand that earnest money is a negotiating tool, not just a formality. Offering above the standard 1%–3% or releasing contingencies early signals financial strength and commitment to a seller reviewing multiple offers. Against cash buyers, a financed buyer with a 5% earnest money deposit and a short inspection period can be just as attractive.

Strategies that work in San Diego's competitive conditions include:

- Increase the deposit amount. Offering 3%–5% on a competitive listing tells the seller you are serious and financially prepared. Savvy buyers in tight markets sometimes go even higher to stand out.

- Shorten contingency periods. Instead of waiving contingencies entirely, compress the timelines. A 7-day inspection period instead of 17 days shows confidence without eliminating your protection.

- Release contingencies early. Once your inspection is complete and your loan is approved, removing contingencies ahead of schedule reassures the seller the deal is solid.

- Combine tactics. Pairing a higher deposit with a shorter inspection window and a pre-approval letter from a local lender creates a package that competes with all-cash offers.

The risk is real. A larger deposit means more money at stake if something goes wrong. Buyers who learn from investor strategies understand how to calculate that risk against the cost of losing a home in a bidding war. Never offer more than you can afford to lose if the deal falls apart outside your contingency protections.

Pro Tip: Pair your increased earnest money offer with a strong purchase offer strategy. Deposit size alone rarely wins a deal. It works best as one part of a complete, well-structured offer.

How to submit and protect your earnest money deposit

The process of submitting earnest money has specific requirements and deadlines. Missing any of them can put your deposit at risk before you even get to inspection.

Escrow agents must receive your deposit within the deadline specified in the contract, typically within 1–3 business days of offer acceptance. A late deposit can be treated as a buyer default. Wire the funds or deliver a cashier's check directly to the escrow company named in the contract. Personal checks are sometimes accepted but verify this with your agent first.

Common mistakes that cost buyers their deposit:

- Missing the deposit deadline. Set a calendar reminder the moment your offer is accepted. The clock starts immediately.

- Wiring to the wrong account. Wire fraud is a real threat in real estate transactions. Always verify wire instructions by calling the escrow company directly using a phone number you find independently, not one from an email.

- Canceling without written contingency removal. If you decide to exit the deal, your agent must submit a written cancellation that references the specific contingency you are exercising. Verbal cancellations do not protect your deposit.

- Letting contingency deadlines expire passively. In California, contingencies do not automatically protect you forever. If you do not actively cancel before the deadline, you may lose your right to exit with a refund.

Keep copies of all deposit confirmations, wire transfer receipts, and escrow acknowledgments. These documents are your proof of timely delivery if a dispute arises. Avoiding common buying mistakes around earnest money starts with treating every deadline as non-negotiable.

Key Takeaways

The earnest money deposit is a performance bond that protects sellers, demonstrates buyer commitment, and is credited toward your closing costs at settlement.

| Point | Details |

|---|---|

| Standard deposit range | Earnest money typically runs 1%–3% of the purchase price, higher in competitive San Diego markets. |

| Applied at closing | The deposit is credited toward your down payment or closing costs, not an additional expense. |

| Contingencies protect you | Inspection, financing, and appraisal contingencies allow a full refund if you cancel before deadlines. |

| California legal nuance | Both parties must initial the liquidated damages clause in the RPA for forfeiture to be the seller's only remedy. |

| Strategic deposit sizing | Offering 3%–5% or more in San Diego can strengthen your offer against competing buyers in low-inventory conditions. |

What I've learned about earnest money after years in San Diego real estate

Most first-time buyers treat earnest money as a checkbox. They ask how much they have to put down, write the check, and move on. That mindset costs people deals in San Diego, where sellers are often choosing between three or four offers on the same weekend.

I have watched buyers lose homes they genuinely wanted because their earnest money was at the floor of what was expected. The seller did not feel confident. Another buyer came in at 4% with a shorter inspection period, and the listing agent called them first. The deposit amount sent a message the first buyer never intended to send.

The flip side is also true. I have seen buyers offer 5% earnest money on a property they had not fully vetted, waive their inspection contingency to look competitive, and then discover a significant foundation issue after closing. The money was not the problem. The missing contingency was. Bigger deposits only make sense when your due diligence is solid.

My honest advice: treat your earnest money decision the same way you treat your offer price. Think about what the seller needs to feel confident, what your financial situation can absorb if something goes wrong, and what contingencies you genuinely need to protect yourself. Those three factors together tell you the right number. A good local agent will know what the current market expects in the specific neighborhood you are targeting. That context matters more than any national guideline.

— Jeff

Ready to make a confident offer in San Diego?

Earnest money strategy is one piece of a larger puzzle when buying in San Diego. Whether you are targeting a condo in Pacific Beach, a single-family home in San Carlos, or an investment property Downtown, the deposit amount and contingency structure in your offer can determine whether you get the call back or not.

Jeffsellssandiego works with first-time buyers and investors across San Diego County, helping clients structure offers that compete without taking on unnecessary risk. Start by browsing current San Diego listings to understand what is available in your price range. When you are ready to talk strategy, the buyer's guide at Jeffsellssandiego walks you through every step of the purchase process, from offer to close.

FAQ

What is earnest money in a home purchase?

Earnest money is a good-faith deposit submitted by the buyer at offer acceptance to demonstrate serious intent to purchase. It is held in escrow and credited toward the buyer's closing costs or down payment at settlement.

How much earnest money is expected in San Diego?

The standard range is 1%–3% of the purchase price, but San Diego's competitive market often sees deposits of 3%–5% or higher on desirable properties. Your agent can advise on current neighborhood norms.

Can you lose your earnest money deposit?

Yes. If you cancel the contract without a valid contingency reason or after contingency deadlines have passed, the seller can keep your deposit as liquidated damages under California contract law.

Does California have special rules about earnest money forfeiture?

California's Residential Purchase Agreement requires both buyer and seller to initial the liquidated damages clause for the seller's retention of the deposit to be the exclusive remedy. Without both signatures, the seller may pursue additional legal damages.

Is earnest money the same as a down payment?

No. Earnest money is paid at offer acceptance and held in escrow. The down payment is paid at closing. The earnest money deposit is applied toward the total cash-to-close, so it reduces what you owe at settlement rather than adding to it.