Home value is defined as the price a willing buyer and seller agree on in an open market, shaped by location, property characteristics, condition, and current economic conditions. To properly explain home value factors, you need to understand what licensed appraisers, mortgage lenders like Fannie Mae, and the broader market actually measure. This article breaks down every major determinant, from Gross Living Area standards to Freddie Mac income data, so you can buy, sell, or plan renovations with clear eyes.

What are the main home value factors?

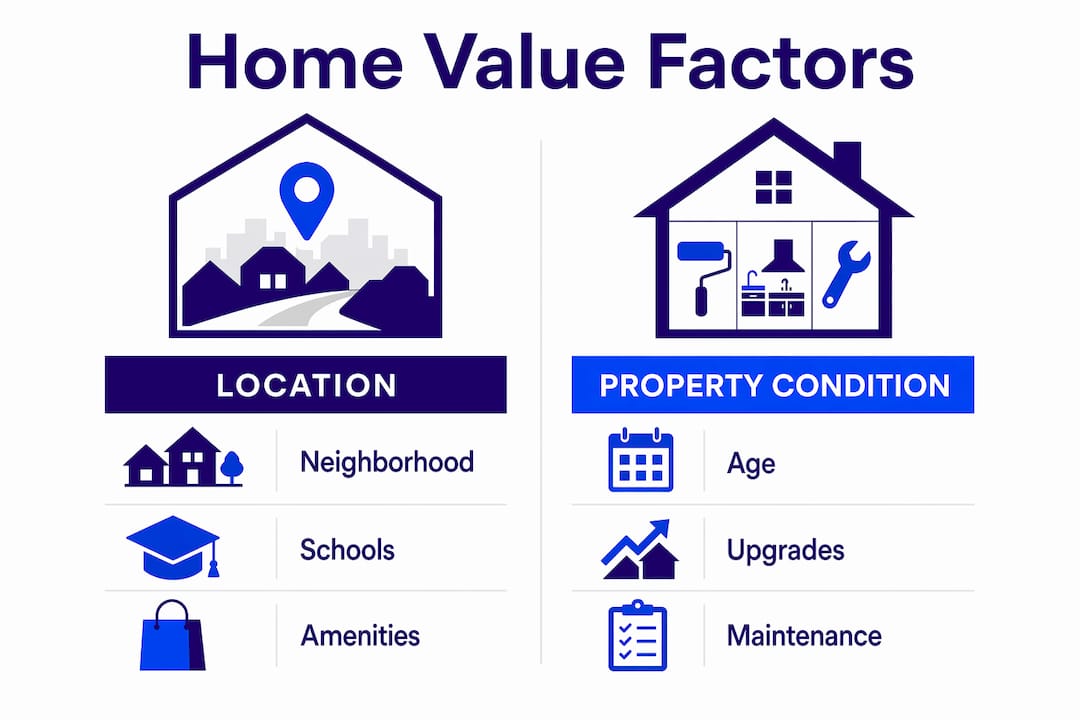

Location is the only permanent value driver because it is beyond any homeowner's control. Neighborhood desirability and school districts set the price ceiling for every home on a given street. You can renovate a kitchen, but you cannot move a house to a better zip code.

After location, property characteristics drive the most variation in price. Appraisers and buyers both weigh these attributes heavily:

- Gross Living Area (GLA): Measured strictly under ANSI Z765 standards, counting only finished spaces above grade. Basements and sunrooms are excluded or valued at a lower rate, which surprises many sellers.

- Lot size: Larger lots add value, but the premium varies sharply by neighborhood and zoning.

- Bedroom and bathroom count: Each additional full bath typically adds more value than a bedroom in most San Diego markets.

- Functional layout: Open floor plans, adequate storage, and a garage all contribute to buyer appeal and appraisal value.

- Condition: Roof age, HVAC functionality, and deferred maintenance all factor into the appraiser's formal condition rating.

Pro Tip: Never assume your finished basement counts toward your home's square footage in an appraisal. Under ANSI Z765, it does not. Price your home accordingly or you risk an appraisal gap at closing.

The condition of a home is scored on a formal scale. Fannie Mae's condition ratings run from C1 (new construction) to C6 (severe deferred maintenance). Condition ratings affect value with real dollar adjustments at every step of that scale. A home rated C4 instead of C3 can lose thousands in appraised value, even if it looks fine to the naked eye.

| Property Feature | Typical Appraisal Effect |

|---|---|

| Updated kitchen and bathrooms | Positive adjustment, highest ROI |

| New roof and HVAC | Positive adjustment, reduces deferred maintenance penalty |

| Finished basement | Valued separately, not included in GLA |

| Poor condition or deferred maintenance | Negative adjustment, C4–C6 rating |

| Garage presence | Positive adjustment, varies by market |

| Highly customized features | Minimal or neutral adjustment |

How do market conditions affect home prices?

Market conditions and economic factors can shift home prices by 10–20% independent of any physical changes to the property. That is a significant swing that has nothing to do with your renovations or curb appeal.

The four biggest external forces on home prices are:

- Mortgage interest rates: When rates rise, monthly payments increase and buyer purchasing power drops. Fewer qualified buyers compete for the same homes, which pushes prices down. The reverse is equally true.

- Local income growth: A 1% increase in per capita income typically corresponds to a 1.5% increase in home prices. San Diego's strong job market in biotech, defense, and tourism directly supports its above-average home values.

- Housing inventory: A seller's market exists when fewer than three months of inventory are available. A buyer's market begins above six months. Inventory levels in your specific neighborhood matter more than national headlines.

- Demographic trends: Population growth, migration patterns, and household formation rates all sustain or weaken demand over time.

Appraisers account for market timing directly. If comparable sales are from six months ago and the market has shifted, a good appraiser applies a time adjustment to reflect current conditions. This is why the date of your appraisal matters, not just the properties used as comparables.

What role do comparable sales play in appraisals?

A home appraisal is a licensed professional's opinion of market value, required by mortgage lenders to confirm the property is worth the loan amount. An appraisal that comes in below the sale price can delay or kill a transaction entirely.

Appraisers build their opinion of value using comparable sales, commonly called "comps." The standard practice is to analyze 3–5 comparable sales within the past six months and within a 0.5 to 1-mile radius. That tight geographic and time constraint exists to reflect the actual market a buyer and seller are operating in.

No two homes are identical, so appraisers make adjustments for differences between the subject property and each comparable:

- Size adjustments: If a comp has 200 more square feet, the appraiser subtracts a dollar amount from that comp's sale price.

- Condition adjustments: A comp in C2 condition compared to your C3 home gets a downward adjustment.

- Amenity adjustments: A comp with a pool, an extra bathroom, or a larger garage gets adjusted to reflect those differences.

- Location adjustments: Even within the same neighborhood, a corner lot, a busy street, or a view can require an adjustment.

Pro Tip: Ask your agent to pull the same comps an appraiser would use before you list or make an offer. If the math does not support the price, you will know before the appraisal does.

A common misconception is that appraisers simply average the comp prices. They do not. Each comp is adjusted individually, and the appraiser reconciles the adjusted values into a final opinion. The process is analytical, not arithmetic.

How do renovations and improvements affect property value?

Renovations affect appraised value only when they align with what buyers in your market actually want. Updated kitchens and bathrooms contribute the highest value among all renovation types. A new roof and HVAC system remove deferred maintenance penalties and can shift a home from a C4 to a C3 condition rating, which carries a real dollar adjustment.

High-return improvements worth prioritizing:

- Kitchen updates: new countertops, cabinets, and appliances that match neighborhood standards

- Bathroom remodels: updated fixtures, tile, and vanities

- Roof replacement: eliminates a major red flag for buyers and appraisers

- HVAC replacement: modern systems reduce buyer risk and improve condition ratings

- Flooring: hardwood or quality LVP over dated carpet

Improvements that rarely recover their cost:

- Elaborate custom landscaping

- High-end finishes in a mid-range neighborhood

- Swimming pools in markets where they are not standard

- Highly personalized design choices that limit buyer appeal

Sellers frequently overvalue their own customized improvements. An appraiser focuses on what the market pays for, not what you paid to install. A $40,000 custom wine cellar in a $600,000 neighborhood adds far less than $40,000 in appraised value. For a practical breakdown of which renovations actually move the needle, the top renovation ROI guide from Jeffsellssandiego is worth reviewing before you spend a dollar.

You can also cross-reference renovation return data with resources like DealAnalyzerAI's renovation analysis to see which project types yield the strongest returns across residential properties.

Pro Tip: Focus renovation dollars on items that appear in appraisal condition adjustments: roof, HVAC, kitchen, and bathrooms. Cosmetic upgrades that do not change the condition rating rarely justify their cost.

Key takeaways

Home value is determined by location, property condition, comparable sales, and market conditions working together. No single factor operates in isolation.

| Point | Details |

|---|---|

| Location sets the ceiling | Neighborhood and school district determine the maximum price any renovation can reach. |

| GLA follows ANSI Z765 | Only above-grade finished space counts; basements are valued separately and often lower. |

| Condition ratings are dollar amounts | Fannie Mae's C1–C6 scale translates directly into appraisal adjustments that affect your sale price. |

| Market conditions shift prices 10–20% | Mortgage rates and local income growth move values independent of any property changes. |

| Renovations must match market standards | Kitchens, bathrooms, roof, and HVAC deliver the strongest return; custom upgrades rarely do. |

What i've learned after years of san diego real estate

Most buyers and sellers come to me focused on the wrong things. Sellers want credit for every dollar they spent on upgrades. Buyers want to negotiate based on cosmetic flaws. Both groups are missing the bigger picture.

Location and market timing are the two factors that move the most money. A well-maintained home in a strong San Diego neighborhood like Point Loma or North Park will outperform a beautifully renovated home in a weaker location every single time. I have watched sellers spend $80,000 on a full remodel and net less than a neighbor who spent $15,000 on targeted updates because the neighbor priced correctly and timed the market.

My honest advice: before you renovate to sell, pull the comps first. If the ceiling in your neighborhood is $900,000 and you are already at $850,000 in condition, a $60,000 kitchen remodel will not get you to $950,000. Appraisers and buyers both know the ceiling. Work with a qualified appraiser or an experienced agent who understands how maximizing your sale value actually works in your specific market.

The buyers who get the best deals are the ones who understand property value factors before they make an offer, not after. Read the comps, understand the condition ratings, and know what the market is doing with interest rates right now. That knowledge is worth more than any inspection contingency.

— Jeff

Ready to know what your san diego home is worth?

Understanding property value factors is the foundation of every smart real estate decision. Jeffsellssandiego works with buyers and sellers across San Diego to translate appraisal data, market conditions, and renovation potential into clear, actionable pricing strategy.

Whether you are searching for your next home or preparing to list, Jeffsellssandiego provides the local market expertise to help you price right and move fast. Browse current San Diego home listings to see how value factors play out across neighborhoods in real time. For sellers, the Seller's Guide walks you through every step of maximizing your home's market position. Contact Jeff directly for a personalized valuation conversation grounded in real San Diego comps.

FAQ

What is the most important factor in home value?

Location is the single most important factor because it is permanent and beyond a homeowner's control. Neighborhood desirability and school districts set the price ceiling that no renovation can exceed.

Does a finished basement count toward home square footage?

No. Under ANSI Z765 standards, appraisers count only above-grade finished space as Gross Living Area. A finished basement is valued separately and typically at a lower rate per square foot.

How many comps does an appraiser use?

Appraisers typically analyze 3–5 comparable sales from the past six months within a 0.5 to 1-mile radius. Each comp is adjusted for differences in size, condition, and amenities before the appraiser reconciles a final value.

Which renovations add the most value before selling?

Kitchen updates, bathroom remodels, roof replacement, and HVAC replacement deliver the strongest appraisal returns. Highly customized upgrades and elaborate landscaping rarely recover their cost in appraised value.

How do mortgage rates affect home prices?

Rising mortgage rates reduce buyer purchasing power, which lowers demand and puts downward pressure on prices. Market dynamics like mortgage rates and job stability can influence home values by 10–20% independent of any property-level changes.