The home appraisal process in San Diego is a licensed appraiser's formal determination of a property's fair market value, ordered by the lender after a purchase agreement is signed but before the loan receives final approval. Appraisals happen after offer acceptance and before closing, making them one of the most consequential steps in any San Diego real estate transaction. The appraiser works through an appraisal management company selected by the lender, not by the buyer or seller. In San Diego's competitive market, where neighborhood desirability and recent sales data shift quickly, the appraisal can make or break a deal.

What are the main steps in the home appraisal process san diego?

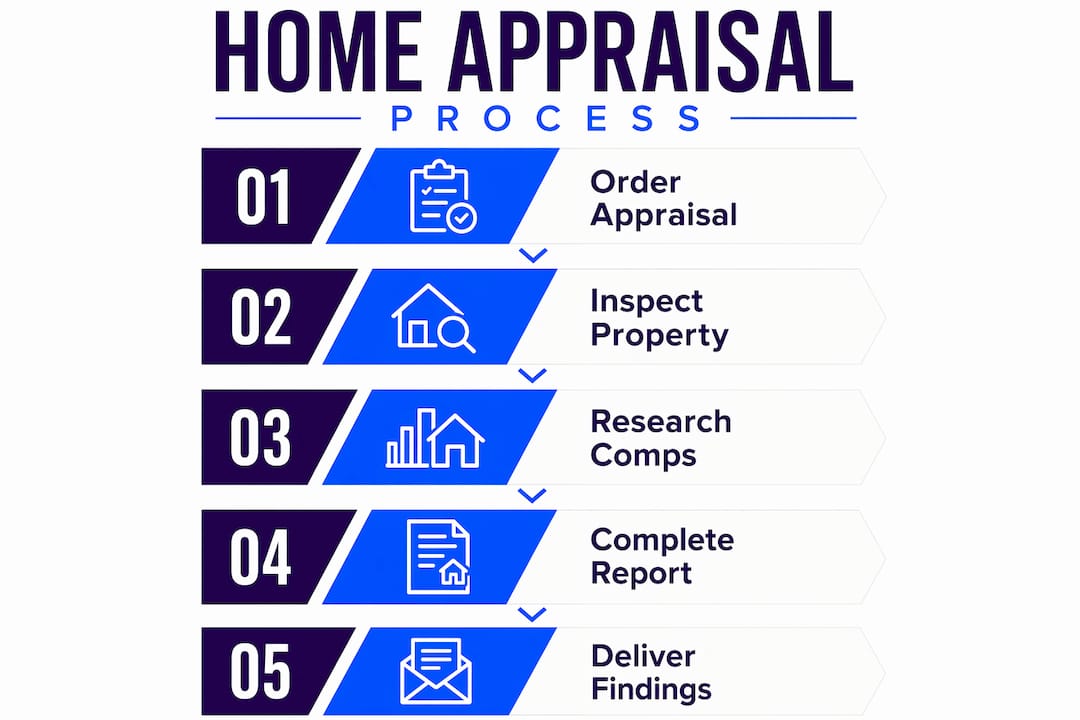

The home valuation process in San Diego follows a clear sequence. Understanding each step helps buyers and sellers avoid surprises and stay on schedule.

Step 1: Lender Orders the Appraisal

Once the purchase agreement is signed, the lender places the order through an appraisal management company. The buyer typically pays the cost of home appraisal upfront, which runs between $550 and $850 for most single-family homes in San Diego County. That fee covers the appraiser's time, research, and written report.

Step 2: Appraiser Schedules and Conducts the Property Inspection

The licensed appraiser visits the property in person. During this visit, they measure square footage, note the number of bedrooms and bathrooms, assess the condition of major systems, and document any upgrades or improvements. The inspection itself usually takes 30 minutes to two hours depending on the size and complexity of the home.

Step 3: Comparable Sales Research

After the visit, the appraiser pulls recent sales data. San Diego appraisers analyze comparable properties adjusted for upgrades, location desirability, and market trends. They typically select three to five comparable sales, called "comps," from the same neighborhood or a nearby area within the past six months.

Step 4: Report Completion and Delivery

The appraiser compiles all findings into a formal written report and submits it to the lender. The buyer's agent receives a copy as well. For conventional loans, the full process from order to delivery typically takes one to two weeks. VA loan appraisals in San Diego can take 30 to 45 days due to additional documentation requirements and stricter property condition standards.

| Appraisal Stage | Typical Timeline |

|---|---|

| Lender orders appraisal | Day 1 after signed agreement |

| Appraiser schedules inspection | Days 2–5 |

| Property inspection | Days 3–7 |

| Comparable sales research | Days 5–10 |

| Report delivered to lender | Days 7–14 (conventional) |

| VA loan report delivery | Up to 30–45 days |

How should you prepare for a home appraisal in san diego?

Preparation separates sellers who get full value from those who leave money on the table. The good news is that most of what appraisers look for is within your control.

- Document every upgrade. Providing information on recent improvements gives appraisers a complete picture to accurately assess market value. Compile receipts, permits, and before-and-after photos for any kitchen remodel, bathroom renovation, new roof, or HVAC replacement.

- Clean and declutter every room. Appraisers are not grading your housekeeping, but a clean, accessible home signals good maintenance. Blocked access to attics, crawl spaces, or electrical panels can slow the inspection.

- Make sure all systems are functional. Test every light switch, run every faucet, and confirm the HVAC operates. Appraisers note deferred maintenance, and those notes affect value.

- Walk the exterior. Peeling paint, broken fencing, or overgrown landscaping all factor into condition ratings. A few hours of yard work can protect thousands in appraised value.

- Work closely with your listing agent. Experienced San Diego real estate agents know which upgrades appraisers value most in specific neighborhoods and can help you present the home strategically.

One distinction worth understanding: the home inspection process in San Diego is separate from the appraisal. A home inspection assesses physical condition; an appraisal determines market value for financing purposes. You need both for most mortgage approvals, but they serve different roles and happen at different points in the transaction.

Pro Tip: Create a one-page "home improvement summary" and hand it to the appraiser at the start of the inspection. List every upgrade with the year completed and approximate cost. Appraisers are required to consider this information, and it takes less than five minutes to prepare.

How does an appraiser determine home value in san diego?

San Diego appraisers follow a methodology grounded in market data, property condition, and location analysis. The process is more structured than most buyers and sellers realize.

The foundation is the sales comparison approach. The appraiser identifies three to five recently sold homes that closely match the subject property in size, age, condition, and location. Each comparable sale is then adjusted up or down to account for differences. A comp with one fewer bathroom than your home gets a positive adjustment added to its sale price. A comp with a newer kitchen gets a negative adjustment. The adjusted values are then reconciled into a single appraised value.

| Factor | Impact on Appraised Value |

|---|---|

| Recent kitchen or bath remodel | Positive adjustment |

| Larger lot size vs. comps | Positive adjustment |

| Older roof or HVAC system | Negative adjustment |

| Busy street or freeway proximity | Negative adjustment |

| School district desirability | Reflected in comp selection |

| Neighborhood sales trends | Affects overall market conditions |

Location carries significant weight in San Diego specifically. A home in Point Loma will be compared only to other Point Loma sales, not to homes in El Cajon. Neighborhood demand, walkability, and proximity to the coast all influence which comps the appraiser selects and how adjustments are made.

Licensed residential appraisers in California must meet Appraiser Qualifications Board (AQB) standards and hold valid state credentials. That credentialing requirement exists to protect buyers and lenders from inflated or deflated valuations. When you hire appraisal services in San Diego, confirming the appraiser's California license is a basic but important step.

"Appraisers rely heavily on local market data, so communicating recent home improvements to your agent ensures appraisers incorporate them into the valuation." — Maxim Real Estate Appraisal

What happens if the appraisal comes in low or high?

A low appraisal is the outcome most buyers and sellers fear. It happens more often in fast-moving markets where offer prices outpace recent comparable sales. Understanding your options before it happens keeps you in control.

- Negotiate a price reduction. If the appraisal comes in below the contract price, the buyer can ask the seller to lower the price to the appraised value. Low appraisals affect financing and contract terms, and sellers who refuse to negotiate risk losing the deal entirely.

- Request a reconsideration of value. The buyer or their agent can submit additional comparable sales to the appraiser and formally request a review. This works best when the appraiser missed a recent sale that supports a higher value.

- Order a second appraisal. If the first appraisal appears flawed, a second opinion from a different licensed appraiser is an option. The buyer pays for this out of pocket, and the lender may or may not accept it.

- Cover the gap in cash. Some buyers in competitive San Diego markets agree in advance to pay the difference between the appraised value and the contract price. This is called "waiving the appraisal contingency" and carries real financial risk.

- Walk away. If the appraisal contingency is in the contract and the parties cannot agree, the buyer can exit the deal and recover their earnest money deposit.

A high appraisal is rarely a problem. It means the buyer is getting the property at or below market value, which strengthens their equity position from day one.

Pro Tip: Before making an offer in a competitive San Diego neighborhood, ask your agent to pull recent comps and estimate the likely appraised value. If your offer price is significantly above those comps, build a cash-gap strategy into your budget before you are under contract.

Key takeaways

A successful appraisal in San Diego depends on preparation, documentation, and understanding the process before it starts.

| Point | Details |

|---|---|

| Appraisal timing | The lender orders the appraisal after the purchase agreement is signed, before loan approval. |

| Cost range | Most San Diego single-family home appraisals cost between $550 and $850. |

| Preparation matters | Documenting upgrades and providing them to the appraiser directly improves valuation accuracy. |

| Low appraisal options | Buyers and sellers can negotiate price, request reconsideration, or order a second appraisal. |

| Inspection vs. appraisal | A home inspection checks physical condition; an appraisal establishes market value for financing. |

What i've learned about san diego appraisals after years in this market

San Diego's real estate market moves fast, and appraisals can feel like the one part of the transaction you have no control over. I disagree with that view entirely.

In my experience working with buyers and sellers across San Diego neighborhoods, the sellers who get the strongest appraisals are the ones who treat the appraiser's visit like a presentation, not a formality. They have a written list of improvements ready. They have pulled their own permits to confirm everything is on record. They have made sure the home is spotless and every room is accessible.

The biggest mistake I see sellers make is assuming the appraiser will "figure it out." Appraisers work from data. If you replaced your HVAC two years ago and never mention it, that upgrade may not show up in the report. If you added a permitted ADU and the appraiser does not have the permit documentation, they may undervalue the addition. You are not gaming the system by sharing this information. You are doing the appraiser's job more accurately.

For buyers, the appraisal contingency is your financial safety net. Do not waive it casually in a bidding war unless you have the cash reserves to cover a gap and you have done the math on comparable sales first. I have seen buyers win offers by waiving contingencies and then face a $40,000 appraisal gap they were not prepared for.

Choose a lender who works with appraisers familiar with your specific San Diego submarket. An appraiser from Riverside County doing a comp analysis in North Park will struggle to find relevant sales and may pull comps that do not reflect local demand. Local knowledge in appraisal services matters more than most buyers realize.

— Jeff

Work with Jeffsellssandiego through every step of the appraisal

The appraisal is one step in a transaction that has many moving parts. Jeffsellssandiego works with San Diego buyers and sellers through every phase, from offer strategy to appraisal preparation to final negotiations.

Whether you are preparing your home to maximize its appraised value or navigating a low appraisal as a buyer, having an experienced local agent in your corner changes the outcome. Jeffsellssandiego provides market-specific guidance, access to San Diego home listings, and hands-on support through the full transaction. Sellers can also use the free home valuation tool to get a baseline estimate before the formal appraisal begins. If you want to prepare your home for top dollar, start with the right local expertise.

FAQ

How long does a home appraisal take in san diego?

A conventional loan appraisal in San Diego typically takes one to two weeks from order to report delivery. VA loan appraisals can take 30 to 45 days due to additional documentation and property condition requirements.

What does a home appraisal cost in san diego?

Most single-family home appraisals in San Diego County cost between $550 and $850. The buyer pays this fee upfront as part of the loan process.

What is the difference between a home inspection and an appraisal?

A home inspection evaluates the physical condition of the property. An appraisal determines the home's market value for mortgage approval purposes. Both are required for most home purchases, but they serve different functions.

Can you dispute a low appraisal in san diego?

Yes. You can submit additional comparable sales and request a formal reconsideration of value from the appraiser. If that fails, ordering a second appraisal from a different licensed California appraiser is another option.

Who selects the appraiser in a san diego real estate transaction?

The lender selects the appraiser through an appraisal management company. Neither the buyer nor the seller chooses the appraiser directly, which protects the independence of the valuation.