Buying your first home in San Diego is exciting, but the numbers can hit hard fast. The median single-family home sits at $1,089,000 as of February 2026, making San Diego the fifth most expensive housing market in the entire country. New owners here spend roughly 86.8% of what renters earn just to cover ownership costs. That's a sobering figure, but it doesn't mean homeownership is out of reach. With the right checklist, local knowledge, and a clear sequence of steps, you can navigate this market with confidence instead of anxiety.

Table of Contents

- What you need before starting your San Diego home search

- Step-by-step San Diego home buying checklist

- Understanding and reviewing legal documents

- Maximizing San Diego homebuyer assistance programs

- The San Diego difference: What most first-time buyers misunderstand

- Take the next step: Expert help for San Diego buyers

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| San Diego home prices | Expect to budget for a median home price of around $1,089,000 and high ownership costs. |

| Critical documents | Always review all required documents and disclosures, especially HOA and title reports. |

| Local assistance programs | Take advantage of down payment and closing cost programs, some providing over $40,000 in aid. |

| Unique market risks | Waiving contingencies is especially risky in older homes—never skip key inspections or disclosures. |

| Expert connections | Work with a local specialist to navigate San Diego’s unique buying process and avoid common pitfalls. |

What you need before starting your San Diego home search

Now that you know having a plan can make all the difference, let's lay the groundwork so you start confident, not overwhelmed.

Set a realistic budget first

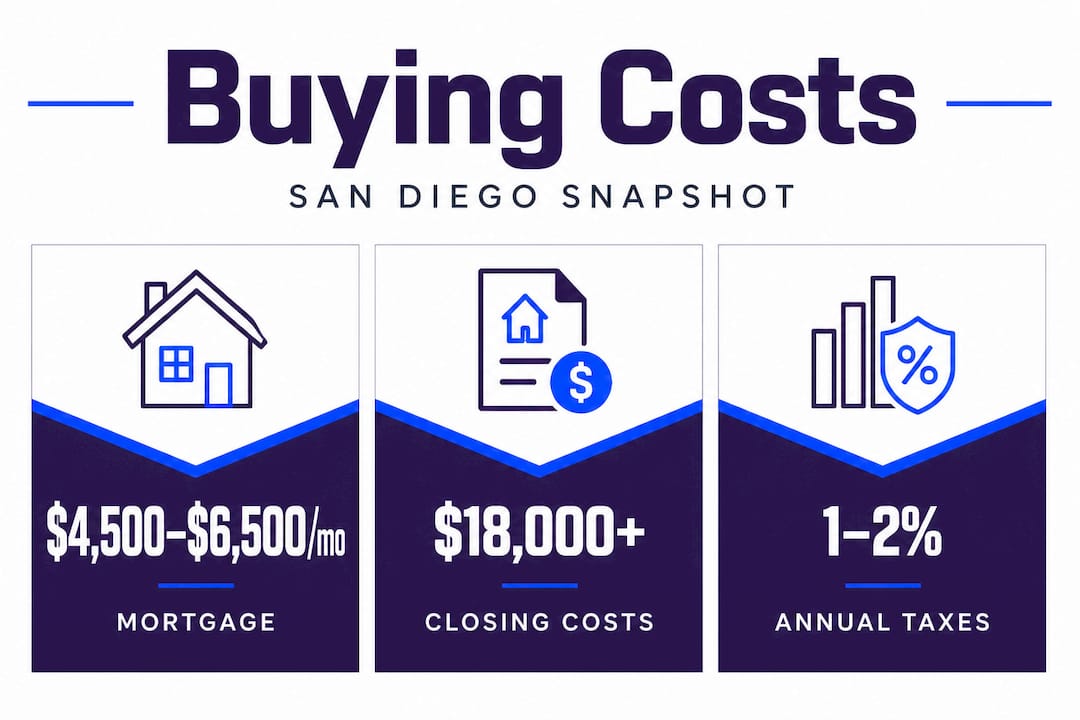

San Diego's 5th most expensive market status means your budget needs to account for far more than just the purchase price. Many first-time buyers focus only on the mortgage payment and get blindsided by the full cost of ownership. Before you tour a single home, sit down and map out every recurring cost.

Here's a breakdown of what to budget for in San Diego:

| Cost category | Typical range | Notes |

|---|---|---|

| Mortgage (principal + interest) | $4,500 to $6,500/mo | Based on 10% down, 7% rate |

| Property tax | 1.1% to 1.3% of value/year | Higher in Mello-Roos districts |

| Homeowner's insurance | $1,200 to $2,500/year | Wildfire zone premiums vary |

| HOA fees | $200 to $800/mo | Common in condos and planned communities |

| Mello-Roos tax | $1,000 to $5,000+/year | Applies to many newer developments |

Understanding the difference between a condo and a house matters enormously here. Reviewing condo vs house costs in neighborhoods like Pacific Beach will show you that condos often carry lower purchase prices but higher monthly HOA fees that can offset the savings quickly.

Know your location priorities

San Diego is not one market. It's dozens of micro-markets, each with its own price range, commute patterns, school ratings, and lifestyle feel. Before you search, write down your non-negotiables:

- Proximity to work or military base

- School district quality (SDUSD vs. Poway Unified vs. Sweetwater, for example)

- Walkability and access to parks or beaches

- Neighborhood vibe (urban, suburban, beach, inland)

- Distance to family or support network

Spend time with a solid San Diego neighborhood guide to compare areas like North Park, Chula Vista, Clairemont, or Santee before committing to a search zone.

Check your income and credit eligibility

Your credit score and income level determine which loan products and assistance programs you qualify for. In San Diego, a score of 640 or higher opens doors to most assistance programs. Conventional loans typically require 620 or better. Pull your credit report early, dispute any errors, and pay down revolving balances to improve your score before applying.

Pro Tip: Gather your last two years of tax returns, two months of bank statements, and your most recent pay stubs before meeting with a lender. This speeds up pre-approval and shows sellers you're serious.

Getting pre-approved is not optional in San Diego's competitive market. Sellers routinely reject offers that arrive without a pre-approval letter. A full underwritten pre-approval carries even more weight than a basic pre-qualification.

Step-by-step San Diego home buying checklist

With your prep in place, here's the San Diego-specific walk-through, from property wish list to closing day.

-

Define your search parameters. Write down your target neighborhoods, minimum square footage, bedroom and bathroom count, and any deal-breakers like no HOA or must-have garage. Be specific but stay flexible on cosmetic issues.

-

Get fully pre-approved. Choose a local lender who understands San Diego's market. A local lender can often close faster than a national online lender, which matters when you're competing against multiple offers.

-

Hire a buyer's agent with local expertise. In San Diego, your agent's neighborhood knowledge can mean the difference between winning and losing a bidding war. Look for someone who actively works the specific areas you're targeting.

-

Start touring homes and asking smart questions. At every open house, ask about the age of the roof, HVAC, water heater, and any recent repairs. Review the questions for open houses that experienced buyers ask to avoid missing red flags.

-

Make a strategic offer. In competitive areas, you may need to offer at or above list price. Your agent should run a comparative market analysis and advise on escalation clauses, seller credits, and terms that make your offer stand out without unnecessary risk.

-

Open escrow and review all documents. Once your offer is accepted, escrow opens immediately. You'll receive a mountain of paperwork. The key legal documents to review include the Purchase Agreement, Escrow instructions, Seller Disclosures (TDS), Title Report, HOA documents, and Natural Hazard Disclosure.

-

Complete all inspections. Schedule a general home inspection, a pest inspection, and a sewer scope. In older San Diego neighborhoods, sewer line issues are surprisingly common and expensive to fix. Never skip the sewer scope.

-

Review inspection results and negotiate repairs. You can request repairs, a price reduction, or a seller credit. Your agent helps you decide what's worth fighting for and what's cosmetic.

-

Remove contingencies strategically. Don't rush to remove contingencies until you're satisfied with inspections and your loan is fully approved. Removing them too early puts your deposit at risk.

-

Final walk-through and close escrow. Do your final walk-through the day before closing to confirm the home is in the agreed condition. Sign your loan documents, wire your closing funds, and get your keys.

Pro Tip: If you're relocating from out of state, use the relocating to San Diego checklist to understand neighborhood basics before you ever set foot in a home.

Here's a quick comparison of offer strategies in different San Diego market conditions:

| Market condition | Offer strategy | Contingency approach |

|---|---|---|

| Hot seller's market | At or above list price | Shorten timelines, keep inspection |

| Balanced market | At list price | Standard contingencies |

| Buyer's market | Below list price | Full contingencies, request repairs |

Understanding and reviewing legal documents

As you move into escrow, reviewing paperwork becomes crucial. Here's what not to overlook.

The volume of documents in a San Diego real estate transaction surprises most first-time buyers. You'll receive hundreds of pages across a 17 to 30 day escrow period. Knowing what to focus on saves you from costly mistakes.

The documents that matter most

The Purchase Agreement and disclosures form the legal backbone of your transaction. Here's what to scrutinize in each:

- Purchase Agreement: Confirm the price, closing date, included items (appliances, fixtures), and all contingency deadlines. Any verbal promise not in this document does not exist legally.

- Transfer Disclosure Statement (TDS): The seller must disclose known defects. Read every line. Vague answers like "unknown" on a 30-year-old home should prompt more questions.

- Title Report: Look for liens, easements, and Mello-Roos districts. A Mello-Roos bond can add thousands of dollars per year to your tax bill and runs for decades.

- HOA Documents: Review the CC&Rs, meeting minutes, and reserve study. Low reserves or pending litigation are serious red flags. Learn more about understanding HOA special assessments before signing anything.

- Natural Hazard Disclosure: San Diego has wildfire zones, flood zones, and earthquake fault lines. This report tells you exactly which risks apply to the property.

- Escrow Instructions: These detail how funds are handled, who pays which fees, and the timeline. Errors here can delay your closing.

Never waive your inspection contingency on a home built before 1980 in San Diego. Older homes in neighborhoods like North Park, South Park, or Golden Hill often have unpermitted additions, original cast-iron sewer lines, and outdated electrical panels. Finding these issues after closing is entirely your problem.

One area buyers consistently overlook is closing costs. Knowing how to save on closing costs in San Diego can put thousands of dollars back in your pocket through negotiated seller credits and strategic lender selection.

Maximizing San Diego homebuyer assistance programs

With your documents in check, the next big advantage is leveraging every dollar of local homebuyer help available.

San Diego has some of the most robust first-time homebuyer assistance programs in California, and most buyers never fully use them. Here's how the major programs stack up:

| Program | Who qualifies | Benefit |

|---|---|---|

| SDHC Low-Income Program | Below 80% AMI (e.g., 1-person: $92,700) | Up to 19% down payment loan + $10K closing grant |

| SDHC Middle-Income Program | 80% to 150% AMI | Up to $40K down payment loan + $10K grant |

| County DCCA Program | Select unincorporated areas | Up to 22% down payment + $10K |

| CalHFA MyHome | Statewide first-time buyers | 3.5% deferred loan for down payment |

The SDHC first-time homebuyer programs are designed to be stacked. For example, a buyer using an FHA loan can combine it with an SDHC deferred loan to cover the down payment and a grant to cover closing costs. This means a qualifying buyer could potentially purchase a home with very little cash out of pocket beyond reserves.

How to maximize your assistance

Here's what you need to do to access these programs:

- Complete a HUD-approved homebuyer education course. This is mandatory for all SDHC programs and takes about 8 hours. Many buyers skip this step and lose access to thousands in assistance.

- Apply early. Funds are limited and allocated on a first-come, first-served basis. Don't wait until you're in escrow.

- Verify your Area Median Income (AMI) level. A single-person household at 80% AMI earns $92,700. A family of four has a different threshold. Know your number before applying.

- Prepare your documents. You'll need tax returns, pay stubs, bank statements, and proof of first-time buyer status (no ownership in the past three years).

- Work with an approved lender. Not all lenders participate in SDHC programs. Confirm your lender is on the approved list before starting your application.

Pro Tip: Attend the homebuyer education session as early as possible in your search, even before you're pre-approved. The session itself often reveals assistance programs and lender contacts you didn't know existed.

The San Diego difference: What most first-time buyers misunderstand

San Diego's homebuying scene plays by its own rules. Here's what sets it apart and what that means for your journey.

The biggest mistake I see first-time buyers make is treating San Diego like Los Angeles or San Francisco. The strategies that work in those markets often backfire here. San Diego has a uniquely high percentage of older housing stock, particularly in central neighborhoods built between the 1940s and 1970s. That means permit history matters enormously.

Unpermitted garage conversions, room additions, and pool installations are extremely common in San Diego. If the seller didn't pull permits, those improvements may not be legal, and your lender may not finance the property as-is. More importantly, you could inherit the liability for bringing those structures up to code after closing. Always ask your agent to pull permit history through the city's online portal.

Waiving contingencies is another area where buyers copy strategies from hotter markets and get burned. In San Francisco, waiving inspections became almost standard during peak years. In San Diego, where homes often have aging sewer laterals and older electrical systems, waiving contingencies on older homes is genuinely risky. A sewer scope that costs $250 can reveal a $15,000 problem. That's not a contingency worth waiving.

The HOA assessments in detail issue is another San Diego-specific trap. Downtown condos and planned communities throughout the county often have underfunded reserves. A special assessment can arrive six months after you close, adding thousands of dollars to your costs with no warning. Reading the HOA's reserve study is not optional.

Finally, the assistance program stacking opportunity in San Diego is genuinely exceptional compared to most California cities. Buyers who attend the mandatory education session, work with an approved lender, and apply early can access tens of thousands of dollars in help. Most buyers I work with don't realize this until it's too late to apply in their current transaction. Don't leave that money on the table.

Take the next step: Expert help for San Diego buyers

Buying your first home in San Diego is one of the biggest financial decisions of your life, and having the right local expert by your side changes everything.

Whether you're just starting to explore neighborhoods or you're ready to make an offer, working with an agent who knows San Diego's micro-markets, assistance programs, and local quirks gives you a real edge. Start by browsing explore San Diego neighborhoods to narrow down your target areas, then search active full home search listings to get a feel for what's available at your price point. When you're ready to go deeper, the San Diego buyer's guide walks you through every stage of the process with local expertise built in. Reach out today and let's build your personalized buying strategy together.

Frequently asked questions

What are the most important documents to review when buying a home in San Diego?

You must review the purchase agreement, all seller disclosures, the escrow instructions, title report, HOA documents, and natural hazard disclosures, as outlined in the legal documents checklist for San Diego buyers.

How much do I really need for a down payment in San Diego?

With assistance programs, qualifying buyers can purchase with as little as 1% to 5% down, and may receive grants up to $10,000 plus secondary loans covering up to 22% of the purchase price through SDHC programs.

Is it safe to waive contingencies when making an offer in San Diego?

Waiving contingencies, especially in older San Diego homes, is risky. Always verify permits, review all disclosures, and complete inspections before removing any contingency protections, per SDHC buyer guidance.

Are there specific local costs or fees unique to San Diego home purchases?

Yes. Buyers should look for Mello-Roos tax districts and HOA reserves or special assessments, which are common throughout San Diego and can significantly increase your true monthly cost of ownership, as noted in the legal documents to review.

What's the average price for a single-family home in San Diego in 2026?

As of February 2026, the median single-family home price in San Diego is $1,089,000, ranking the city fifth among the most expensive housing markets in the United States.